Debt Collector Calling About a Personal Loan? Your Rights

Borrower RightsA rights-first walkthrough of FDCPA and Regulation F protections, plus the three letters that shift leverage and the lines collectors say that are not true.

TrustPointLoans helps point you toward loan options that align with your financial situation & funding needs.

We use 256-bit SSL technology to encrypt your data.

Disclosures

We line up lender types against the things underwriters actually care about.

Our soft-pull form takes 60 seconds. No email required, no impact on your credit score.

We sort lender types by who actually approves your situation - credit profile, income, debt-to-income.

Pick the offer that fits and finalize directly with the lender. Funds can land as soon as the next business day.

Plain-spoken guides on personal loans, debt, and credit - written by people who've actually borrowed.

A rights-first walkthrough of FDCPA and Regulation F protections, plus the three letters that shift leverage and the lines collectors say that are not true.

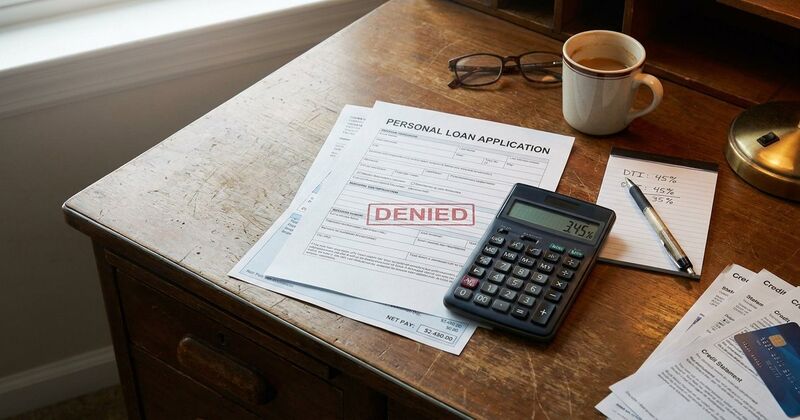

The difference between pre-qualified, pre-approved, and approved, plus the seven specific reasons a pre-approval flips to a denial at full underwriting.

An ex-underwriter walks through the seven real reasons a steady-job, decent-income borrower gets denied for a personal loan, and what to do about each.

The five most common ways a debt consolidation loan grows the problem instead of solving it, and how to tell which version of the borrower you actually are.

Complete one simple form to explore loan options tailored to your financial profile. No hard credit pull required.

Get Started →Quick answers before you start a request. Still unsure? Contact us and we will help.

We are a matching service. You tell us what you need, we point you toward lenders in our network whose underwriting tends to fit your situation, and the lender takes it from there. We are not a lender, a broker, or a financial advisor.

No. Checking your options here uses a soft credit check, which does not affect your score. A hard inquiry only happens if you choose to formally apply with a specific lender after seeing your matches.

Yes. Our network includes lenders that work with thin files, lower scores, self-employed income, and people consolidating debt while they rebuild. Approval is never guaranteed, but you will see options that have a real chance instead of only ones built for 740+ borrowers.

A couple of minutes. You will be asked for the loan amount, purpose, ZIP code, and basic income information. No 30-page application, no upfront documents, no account to create.

We serve borrowers across the United States, but lender availability varies by state because rates, fees, and licensing rules differ. The matching screen will show you which lenders in our network can work with your state and situation.

It is encrypted in transit, used to find lenders that fit your request, and shared only with the lenders you are matched with. We do not sell your data for marketing lists.

Not at all. Seeing your options is free and carries no obligation. You decide whether to move forward with a formal application with any specific lender. Nothing is locked in until you sign loan documents directly with the lender.