Quick answer: Call people in this order: the shop (for a payment plan or in-house financing), your employer (for an earned wage advance or hardship loan), your local Community Action Agency, your credit union (for a Payday Alternative Loan), and only then an online personal lender. Skip payday and title loans entirely if you can. The order matters more than the speed.

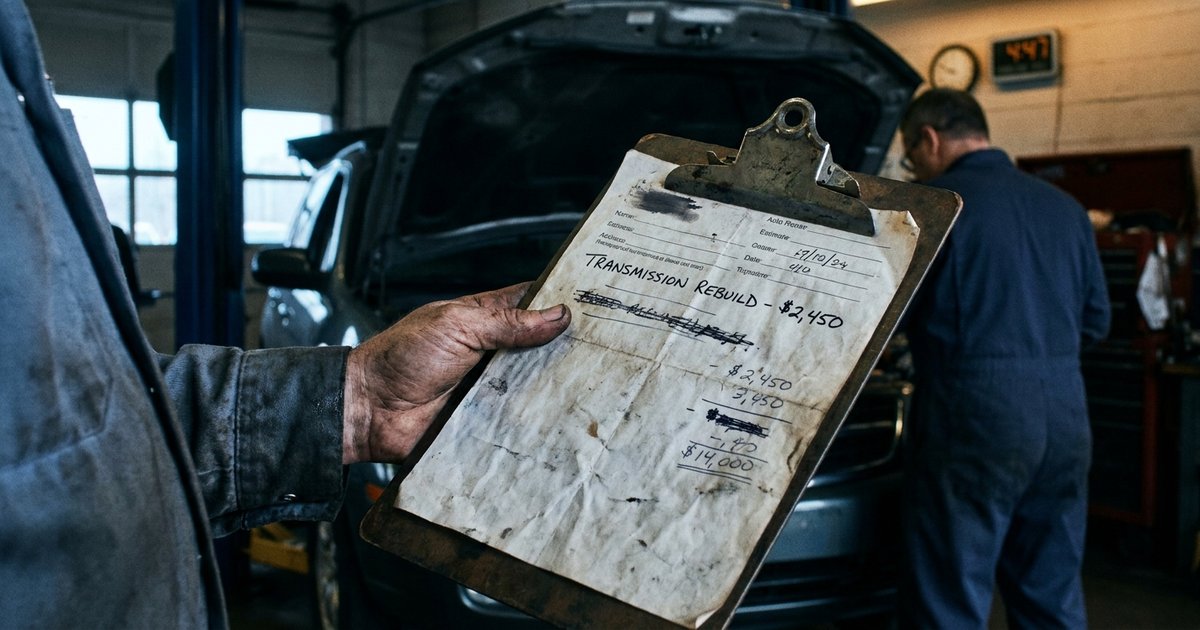

The shop calls at 4:47 on a Tuesday. Transmission. Fifteen hundred dollars. They want a deposit by Friday or storage fees start, and you drive for a living. You have three days, a paycheck that hits next Friday (not this one), and a checking account that would not survive a $400 surprise without an overdraft. That is the situation this piece is written for.

The Federal Reserve's 2024 Survey of Household Economics and Decisionmaking found that 37 percent of US adults could not cover a $400 emergency expense from cash alone. Thirteen percent said they could not cover it at all. A $1,500 repair sits well past that line for tens of millions of people. So the question is not whether to borrow. The question is which order to call people in, and what each option actually costs.

What follows is sorted by speed and total cost, not just one or the other. Most "fast cash" articles ignore what the money costs you. Most "best emergency loan" articles ignore that you needed it yesterday. You need both filters at the same time.

Hour 0: Stop the bleeding before you borrow anything

Before you go anywhere near a loan, do three things at the shop.

Get a written estimate, line-itemed, with parts and labor separated. Ask whether they can hold the car without storage fees if you commit to the repair and put down a partial deposit. Ask whether they offer their own payment plan or work with a third party like Sunbit or Affirm at the service counter. Many independent shops and chains (Pep Boys, Midas, some local transmission specialists) will run you through a 90-day or 6-month financing option that, for borrowers with fair credit, beats anything you can arrange in 72 hours from the outside.

That single conversation can knock the urgency from "Friday or else" to "Friday for the deposit, the rest in installments." It changes what you have to find by Friday from $1,500 to maybe $300.

Hours 1 to 6: The free and almost-free tier

Call these in this order.

Your employer. Ask HR or your manager whether the company offers an earned wage advance, a paycheck advance, or a hardship loan. Walmart, Target, Amazon, and a long list of mid-size employers run programs through DailyPay, PayActiv, or Even. The fee is usually a few dollars per advance, sometimes nothing if you accept next-day funding instead of instant. This is not a loan. It is your own already-earned money, paid early.

Your local Community Action Agency. There are roughly 1,000 of these across the country, funded in part through LIHEAP and Community Services Block Grants. They keep discretionary crisis funds for exactly this kind of situation, especially when the broken thing is the way you get to work. Find yours through the Community Action Partnership directory. Disbursement is typically 24 to 72 hours, sometimes faster, often direct to the shop.

Your credit union, if you already belong to one. Ask specifically about a same-day signature loan or a Payday Alternative Loan (PAL). PAL I caps at $1,000 with a 28% APR and a $20 max application fee. PAL II goes up to $2,000 over 12 months under the same APR cap. If you joined the credit union recently, ask about PAL II specifically, because the old 30-day membership waiting period was eliminated.

Family, in writing. If you are going to ask, ask for a defined amount with a defined repayment date and put it in a one-page note both of you sign. The IRS does not care about a $1,500 family loan, but your relationship will care if the terms are vague. A simple note with the amount, the date borrowed, the repayment schedule, and both signatures protects everyone.

Hours 6 to 24: Tools you already have

If the free tier did not close the gap, the next tier uses credit you already qualify for.

A 0% APR purchase you can pay off in three to six months on an existing credit card, used at the repair shop, is almost always cheaper than a new short-term loan. Read the terms before you swipe: deferred-interest cards (common in store-branded auto financing) charge you all the back interest if you miss the payoff window by a single day. Real 0% APR purchase windows on a general-purpose card do not.

Cash advance apps like EarnIn, Dave, Brigit, and MoneyLion can move $100 to $750 to a debit card the same day. Read the actual fee structure carefully before you agree. The "instant" fee is usually a few dollars; the "tip" is optional, no matter how the screen is designed; and the repayment auto-pulls on payday, which can collide with your rent or your car insurance debit if you do not plan for it. Treat the funding date and the auto-pull date as two different problems to solve.

24 to 72 hours: Online personal loans

Several online personal lenders advertise "same-day funding," which in practice is usually next-business-day funding because of bank cutoffs. If you apply Tuesday afternoon, money typically lands Wednesday or Thursday. That works for a Friday deadline. It does not work for a Wednesday one.

What to look for, in order:

- The APR (not the monthly payment, not the "rate") in writing, including any origination fee.

- The total of payments over the life of the loan, also in writing. The Truth in Lending Act and Regulation Z require both numbers in the disclosure before you sign.

- No prepayment penalty. You want the option to pay this thing off as fast as possible.

- The funding timeline confirmed in writing, not just on the marketing page.

For a borrower with a credit score in the high 600s or above, online personal loan APRs in the current environment commonly run 10% to 25%, in line with Bankrate's national rate tracker. With damaged credit, that range pushes well past 30% and toward the legal cap in your state. At those rates, you should be running the math against a PAL II at 28% before you sign anything.

The last resort tier (and the math nobody shows you)

Payday loans, title loans, and "easy approval" installment loans are last resorts because the math is brutal and the trap is real. The CFPB's payday loan explainer pegs the typical fee at $10 to $30 per $100, which works out to roughly 400 percent APR on a two-week loan. A $400 payday loan rolled over a few times can cost more in fees than the original principal inside six months. (We walk through the full rollover math in how a $400 payday loan becomes $1,800 in six months.)

A title loan is worse, because the collateral is the same broken-down car you are trying to fix. If the repair fails or the loan does, you lose the vehicle that was supposed to make you the money to repay it. The Center for Responsible Lending has tracked title-loan repossession rates around one in five borrowers in some states. That is not a tail risk. That is a coin flip with a thumb on the scale.

Twenty states plus DC cap small-loan APRs near 36%, according to NCLC's predatory installment lending report. The Military Lending Act caps most consumer credit to active-duty servicemembers and their dependents at 36% Military APR. Outside those guardrails, you are on your own. (Our state-by-state APR cap guide shows you which protections actually apply where you live.)

What not to do

Do not take a title loan against the vehicle currently in the shop. Do not take a second short-term loan to pay off the first one. Do not take a cash advance against a credit card that is already near its limit, because the cash advance APR is usually higher than the purchase APR and there is no grace period: interest accrues from day one. And do not wire money to anybody who calls you and says you are "pre-approved" for a loan you never applied for. That is not a lender. That is the start of an advance-fee scam, and our walkthrough on spotting a fake lender before you send money covers the playbook.

The 90-day rebuild

Once the car is back on the road and the dust settles, the next job is a buffer. A $500 starter emergency fund is enough to absorb most of the next surprise without sending you back through this article. Automate $20 a week into a separate high-yield savings account at a different bank than your checking. In 25 weeks you have $500 plus a small amount of interest, and you have not thought about it once.

If $20 a week is not realistic, start with $5. The point is the habit and the separate account, not the speed.

How Trust Point Loans fits an emergency

We are not a lender, broker, or financial advisor. We help borrowers think through which type of funding actually fits their situation, and we publish material like this so the order-of-operations is clear before the panic starts. Rates, terms, fees, and approvals are set by lenders themselves and depend on your credit profile, your state, and the lender's underwriting.

If you are reading this at 4:48 on a Tuesday with the shop on the other line, the short version is: ask the shop first, your employer second, your credit union third, and a payday storefront last. The order matters more than the speed.

Common questions about raising emergency cash fast

How fast can I actually get $1,500 from a personal loan?

For a borrower with established credit applying to an online lender, funds typically arrive the next business day after approval. "Same-day funding" claims depend on bank cutoffs and ACH timing, so plan for next business day unless the lender confirms otherwise in writing.

Is a Payday Alternative Loan really capped at 28%?

Yes. The NCUA caps PAL I and PAL II at 28% APR with a maximum $20 application fee. PAL I covers $200 to $1,000 over 1 to 6 months. PAL II goes up to $2,000 over 12 months. You have to be a member of a federal credit union that offers them.

Can my employer legally advance my paycheck?

Yes. Earned wage access is offered through programs like DailyPay and PayActiv, and many large employers have hardship loan programs. Ask HR directly. Some states (California, New York) have started treating certain advance products as loans, which adds disclosure requirements but does not block the option.

Is a title loan ever the right answer?

Almost never, especially when the car is the source of income. The Center for Responsible Lending has documented repossession rates around 20% in some states, and the APR is comparable to payday-loan territory. The collateral risk is the deal-breaker.

What if I have already taken a payday loan and cannot pay it back?

Many states require payday lenders to offer a free Extended Payment Plan on request. Federal credit unions can sometimes refinance the debt into a PAL II at 28% APR. Nonprofit credit counselors accredited by the NFCC or FCAA can negotiate a debt management plan. The CFPB complaint portal is the right place to escalate if a lender refuses to follow state rules.