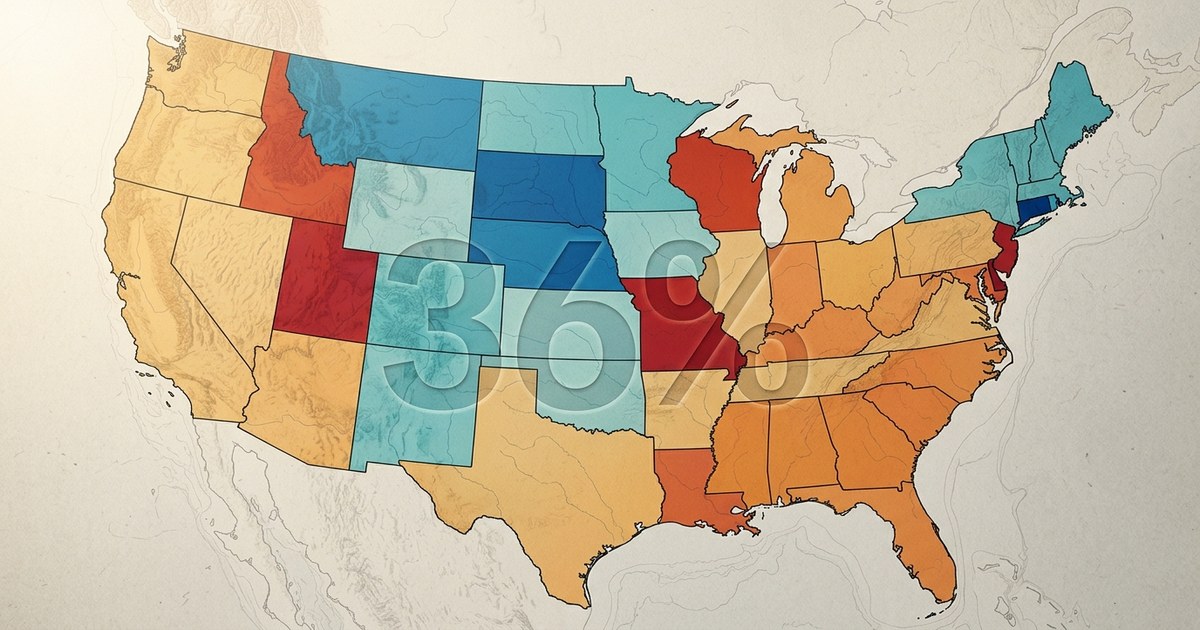

Quick answer: 45 states and DC cap interest on at least some consumer installment loans, but the strength varies wildly. Connecticut, Montana, South Dakota, and Nebraska enforce 36 percent all-in caps. Delaware, Missouri, Idaho, Utah, and Wisconsin leave at least one loan-size category effectively uncapped, where APRs above 200 percent are legal. Your ZIP code is one of the biggest single variables in your loan offer.

Two borrowers with the same credit score, the same income, and the same debt-to-income ratio can apply to the same online lender on the same day and see APRs that differ by more than 100 percentage points. The only thing that changed is the state on the application. According to the National Consumer Law Center's predatory installment lending in the states report, 45 states and DC cap interest and fees on at least some consumer installment loans, but the strength of those caps varies wildly. In Connecticut, Montana, and South Dakota, a $500 small-dollar loan tops out at 36 percent APR all-in. In Missouri, the same product can carry an APR over 200 percent. That is not a typo.

Your ZIP code is, in practical terms, one of the biggest variables in your loan offer. Here is how the rules actually work, where the strong caps are, where the loopholes live, and what you can do about it if you live in a state with weak protections.

Why your state matters more than most borrowers realize

State usury laws set the maximum APR a non-bank lender can charge a resident. Federal law mostly defers to those state rules for installment lending, with two big exceptions: the Military Lending Act (a flat 36 percent MAPR cap for active-duty servicemembers and their dependents nationwide), and federal preemption for national banks under the Marquette doctrine, which lets a national bank export its home-state interest rules to other states.

That second exception is why you will notice so many online lenders are technically headquartered in Delaware, Utah, or South Dakota. Those states have permissive lending environments that allow nationally chartered partner banks to lend across state lines at rates that would be illegal if originated by a state-licensed lender in your own state. The arrangement is sometimes called a "rent-a-bank" partnership, and it is contested in court. Several states (Colorado and DC, among others) have brought enforcement actions against specific structures. None of that has been fully settled.

What this means in practice: when you apply online, the lender's licensing and the bank partner sitting behind it determine which rate ceiling actually applies to you. Sometimes that is your state cap. Sometimes it is the partner bank's home-state ceiling. The difference is real money.

The 36 percent benchmark, and where it came from

Why 36 percent? It is not arbitrary. The 36 percent APR limit traces back to early 20th-century uniform small-loan laws and was reaffirmed by Congress in 2006 when the Military Lending Act set 36 percent as the federal ceiling for active-duty borrowers. NCLC and most consumer-finance researchers treat 36 percent as the threshold above which small-dollar loans tend to function more like debt traps than like credit.

Several states have put 36 percent caps in place by ballot initiative rather than legislation, which tells you something about how these policies tend to perform when voters get a direct say:

- Montana: 36 percent cap, voter-approved in 2010.

- South Dakota: 36 percent cap, voter-approved in 2016.

- Nebraska: 36 percent cap on payday loans, voter-approved in 2020.

- Colorado: 36 percent cap on payday loans, voter-approved in 2018.

- Arizona: 36 percent cap on payday loans, voter-approved in 2008.

Each of these passed with strong bipartisan margins, often above 70 percent. Voters across the political spectrum tend to agree on this one.

States with the strongest borrower protections

Per NCLC's 2025 report, the following states have comprehensive 36 percent (or lower) APR caps that include most fees and apply across small-dollar and mid-size installment loans. The exact loan-size brackets covered vary, so always check the regulator before signing:

- Connecticut. Strong all-in caps across loan sizes.

- Montana. 36 percent across small consumer loans.

- South Dakota. 36 percent, no exceptions for licensed lenders.

- Nebraska. 36 percent on payday-style loans.

- Vermont, New Jersey, New York, Massachusetts. Long-standing low usury caps in the 16 to 25 percent range for many loan types.

If you live in one of these states and you are seeing online offers above the cap, that is a signal worth investigating. Either the lender is operating through a bank partnership that may or may not be enforceable in your state, or the offer is not legally extendable to you and the rate will change at underwriting. Either way, treat it as a flag, not a deal. (When the offer feels too good, our walkthrough on how to spot a fake lender before you send money covers the next layer of risk.)

States with weak or no caps on at least one loan-size category

This is where the math gets ugly. NCLC identifies the following states as having no APR cap on at least one consumer installment loan size:

- Delaware

- Missouri

- Idaho

- Utah

- Wisconsin

In these states, NCLC's $500 installment loan analysis shows APRs that can clear 200 percent and, in some product categories, push past 300. A handful of other states cap larger loans but leave small-dollar loans (under $1,000 or $2,000) effectively uncapped. The result for borrowers in cap-free states is an offer landscape dominated by high-cost subprime installment lenders, because the legal headroom exists.

If you live in one of these states, the loan products that show up in your search results are not the same products a borrower in Connecticut sees. That is not paranoia. That is geofenced underwriting working as designed.

The rent-a-bank workaround, in plain English

An online installment lender wants to charge 89 percent APR. Your state caps non-bank lenders at 36 percent. The lender partners with a small bank chartered in a permissive state. The bank "originates" the loan, then sells it (or sells the right to service and collect on it) back to the online lender. Because the originator is a bank protected by federal preemption, the argument goes, the rate ceiling that applies is the bank's home state, not yours.

State attorneys general have pushed back against this in court. Outcomes have been mixed. The CFPB and FDIC have both signaled, at various points, that they consider the structure suspect when the non-bank partner is the "true lender" in economic substance. None of that means the loans are illegal in your state, and none of it means a borrower should self-litigate. The point is awareness: if your offer comes from a lender headquartered in Delaware or Utah, the rate you see may be legal under that lender's framework but well above what a state-licensed lender could charge you.

The junk-fee loophole inside "cap" states

Even in 36 percent cap states, the cap may not include every charge. NCLC has flagged that some states' caps exclude credit insurance premiums, processing fees, and origination fees from the APR calculation. A loan stated at 35.99 percent APR can carry an effective all-in cost well above that once those add-ons are included.

The protective move is simple: pull the TILA disclosure, look at the APR (which by law must include finance charges), and compare it to the total of payments. If the total of payments is dramatically higher than what a 35.99 percent calculation would produce, fees outside the APR are doing the work.

What to do if you live in a cap-free state and need a loan

If your state does not give you a meaningful APR ceiling, the answer is not "borrow at 199 percent because that is what is on offer." The answer is to step out of that channel entirely. Your options:

- Federal credit unions. Capped at 18 percent APR for most loan types under the NCUA's federal usury ceiling, regardless of your state. Most credit unions also offer a Payday Alternative Loan (PAL) program with a 28 percent APR cap.

- Community Development Financial Institutions (CDFIs). Mission-driven lenders that price small-dollar credit closer to mainstream rates. The CDFI Fund's Locator at the U.S. Treasury site lets you find one near you.

- Employer-based loan programs. A growing number of employers offer payroll-deducted small-dollar loans through providers like TrueConnect and Salary Finance. Rates typically run 20 to 30 percent and reporting is positive to credit bureaus.

- Secured loans. A share-secured or auto-secured loan at a credit union shifts the risk profile dramatically and brings APR down with it.

- State and local emergency assistance. Not a loan, but worth checking before borrowing at triple-digit rates. 211.org maintains a state-by-state directory. (For a full sequence on raising emergency cash, see our 72-hour emergency cash playbook.)

If you have already taken out a high-APR loan in a cap-free state and you are struggling, contact a nonprofit credit counselor accredited by the NFCC or FCAA. If you suspect the loan violated your state's rules (as opposed to simply being expensive), legal aid is the route, not a DIY dispute. The Legal Services Corporation directory lists free legal aid by location.

How to verify your state's actual rules in two minutes

Three sources, all free:

- NCLC's State APR Cap Fact Sheet. Updated annually; shows current caps for $500, $2,000, and $10,000 installment loans.

- Your state's Department of Banking or Financial Regulation. Every state has one. Search "[your state] department of banking consumer loan."

- NMLS Consumer Access (nmlsconsumeraccess.org). Confirms whether a specific lender is licensed to operate in your state and shows any disciplinary actions.

Why state APR caps matter for your loan

The same lender, the same product, and the same applicant can produce wildly different APRs based on a single line on a form. Knowing which ceiling protects you, which loophole may be doing the opposite, and which alternative channels exist outside the high-APR retail market is the difference between paying 28 percent on a credit union PAL and paying 199 percent on an online installment loan that is technically legal in your state. The legal does not always equal the affordable. Your job as a borrower is to know which one you are signing.

Common questions about state APR caps

What is the 36 percent APR cap?

The 36 percent APR cap is the rate ceiling NCLC and most consumer-finance researchers identify as the threshold for sustainable small-dollar credit. It is also the federal cap under the Military Lending Act for active-duty servicemembers and their dependents. Several states (Montana, South Dakota, Nebraska, Connecticut) apply 36 percent caps to civilian borrowers as well.

Which states have the strongest personal loan APR caps?

According to NCLC's 2025 report, Connecticut, Montana, South Dakota, Nebraska, Vermont, New York, New Jersey, and Massachusetts have some of the strongest comprehensive caps, generally at or below 36 percent on small-dollar installment loans. Exact coverage varies by loan size.

Which states have no personal loan APR cap?

Delaware, Missouri, Idaho, Utah, and Wisconsin have no APR cap on at least one consumer installment loan size category. Other states are partially uncapped depending on loan size.

Can a lender in another state charge me more than my state's cap?

Sometimes, through "rent-a-bank" partnerships in which a federally chartered bank in a permissive state originates the loan. These structures are legally contested, and outcomes vary by state. The Military Lending Act caps APR at 36 percent for active-duty servicemembers regardless of state.

How do I check my state's current APR rules?

Use NCLC's state cap fact sheet, your state Department of Banking, and NMLS Consumer Access (nmlsconsumeraccess.org) to verify both the rule and the lender's licensing. State laws update regularly, so always confirm before signing.